In the first post, I asked whether a business can be run democratically. That question came into focus during our B Corp certification process, which pushed us to think harder about voice, participation, and who gets to help shape the company.

It is one thing to talk about shared governance in general. It becomes more concrete when you have to decide how capital gets used. Every company has to decide how much stays in reserve, how much goes back into investing in the future, and how much supports current operations or eventually shows up in raises, bonuses, or profit share. That is capital allocation.

The tradeoffs that arise are not theoretical. For example, money that goes into R&D does not show up somewhere else that year. Cash held in reserve buys stability, but too much cash can also mean you are not putting resources to work. Higher near-term profit can reflect discipline. It can also mean you are underinvesting in the future.

In 2025, 22 cents of every dollar we made went to R&D. That is the highest level of R&D investment we have made. I do not see that as the permanent ratio going forward. Part of what happened is that we are playing catch-up. Looking back, I think we underinvested in R&D for a period of years, and that left us without enough fuel for the next round of growth. So this recent push is not just a general argument for spending more. It is also a correction.

Over time, investment should produce stronger growth, healthier margins, more operating profit, more resilience, or some combination of those. Otherwise it is just spending with a story attached to it.

That does not mean every investment can be tied neatly to one short-term metric. R&D often takes time to pay out. But it does mean we should be able to explain what return we expect, what time horizon we are working with, and what evidence would tell us the investment is making sense.

A team member looking at a capital-allocation vote is not judging R&D in the abstract. They are weighing it against their own compensation, future profit share, staffing, operating needs, and the overall health of the business. They are also asking a fair question: do we see enough progress from this investment to keep supporting it at this level?

And if we change that allocation, what follows from it? Does a lower R&D number simply mean tighter discipline? Does it mean slower product development? Does it affect staffing? These choices shape people’s work and the future of the business at the same time.

This is one of the places where democratic governance has to mean something. I do not think every operating decision should become a vote. Team members need autonomy in their own areas of responsibility, and leadership still has to execute. But some choices matter enough to the direction of the business that they should not be made only at the leadership level without discussion.

If we are going to ask people to weigh in on capital allocation,how do we make that input useful? People need enough context to understand the tradeoffs and enough structure to see what choice is actually in front of them, without needing a full accounting education.

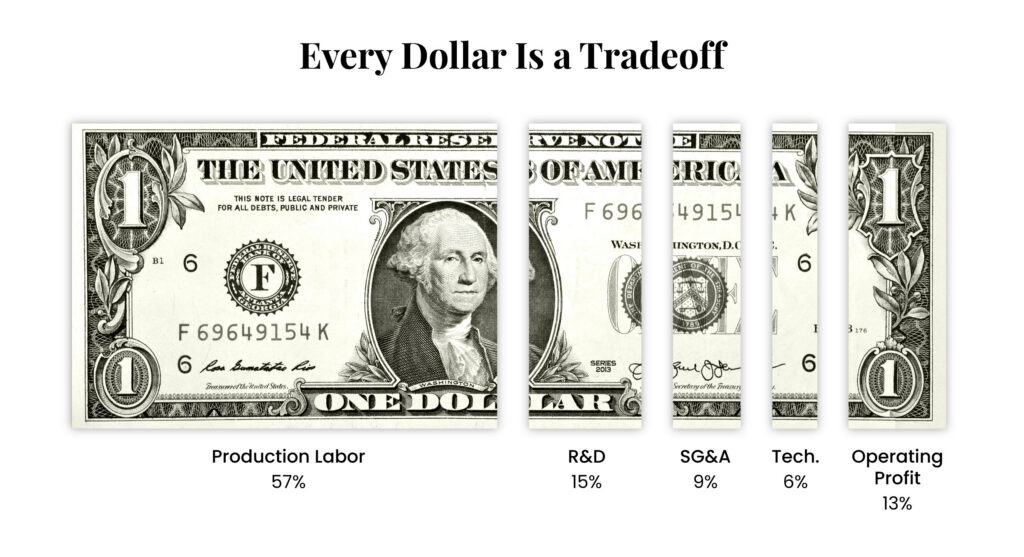

One tool that has helped open this discussion is the common-size financial statement. In recent all-hands meetings, I’ve started using them for exactly that reason. Instead of handing people a pile of dollar figures, they restate the business in proportions. Out of every dollar of revenue, how many cents went to R&D? To labor? To operating costs? It is often a more usable way to look at the business because it lets people compare priorities and patterns without getting lost in scale.

Cash visibility belongs in that picture too. A company can look healthier on an accrual basis than it feels in operation. Revenue may be booked before it is collected. Some invoices take time to turn into cash. Some never do.

To make this concrete: we maintain an internal policy that defines what happens when our days of cash on hand move outside a target range of 90–120 days. The triggers are evaluated on a rolling window; one trailing month of actuals plus three months of projections, so the analysis stays grounded in real numbers rather than compounding forecast error over a full year. When cash drops below the target, the process asks a specific set of diagnostic questions: how much was business contraction, how much was controllable spending, how much was intentional R&D investment, how much was utilization. When cash runs high, it asks the mirror image: is this outperformance, underspending, unfilled roles, or just timing? In both cases, the analysis goes to the leadership team for a decision.

Cash on hand, existing obligations, debt, and other operating guardrails tell you what can responsibly be proposed in the first place. They do not decide what the company should prioritize. They show where the actual constraints are.

Open-book management helps make the business legible, and it is the approach we’ve taken for years. The goal is not transparency for its own sake. It is to give people enough financial and operating information to make real choices instead of voting on instinct. We have always asked for this kind of input, and people on the team have asked great questions over the years when we walk through financial performance. They have also caught mistakes I’ve made. That is part of the point.

The goal is not transparency for its own sake. It is to give people enough financial and operating information to make real choices instead of voting on instinct.

What we need is a process where people are weighing real choices, within the constraints of the business. Team members need enough visibility into how things work to make that useful. And the choices themselves have to be clear enough that, at the end of it, we can actually do something with the result.

My guess is that the process will need a broader discussion period up front and a narrower final vote at the end. That raises a few practical questions. What belongs on the ballot: profit targets, reinvestment ranges, reserve levels, directional priorities, something else? How much financial context does someone need in order to participate well? What kind of discussion helps people think clearly instead of just generating more noise? The next post will focus on those questions, and on what we included on the ballot.

Shilo Jones is the co-founder of StatBid and Poolaroo. Over the past 30 years, he’s built e-commerce businesses and helped merchants grow across multiple categories, with plenty of lessons earned the hard way. At StatBid and Poolaroo, the work is team first and operator led. Poolaroo functions as a living laboratory where we run experiments on our own dime, learn fast, and turn those lessons into practical wins we can share with more merchants. Shilo’s long term focus is sustainable commerce by 2050: thriving wages, circular products by design, and carbon neutral logistics.